Quarter1

23

f e a t u r e

{

being readable. Tokenization eliminates the need to refer to a

customer card number for returns, voids, card on file, and recurring

transactions. Both E3 and tokenization combine with EMV to

provide optimal transactions.

How Are EMV Transactions Authorized?

EMV transactions can be authorized online and offline. EMV

transactions authorized online are verified though an online

connection from the merchant’s terminal or point-of-sale system to

card issuers, via an acquirer like Heartland Payment Systems. This

process is much like today’s magnetic stripe-based transactions in

the U.S., where transactions are authorized online. EMV offline

transactions are authorized through authentication of the card and

the merchant EMV acceptance device (point of sale or terminal).

MasterCard and Discover have announced their support for offline

authorization, but Visa does not support offline authorization for

U.S.-issued chip cards. Chances are that your transactions will be

authorized in an online mode and you will not need to be concerned

about offline authorization.

Tip Management with EMV

While EMV dual message transactions will still allow tip

adjustments when used as a “chip and PIN,” restaurants will want

to streamline EMV card acceptance. Operationally, the following

might be a best practice:

•

When an EMV card is tendered and a PIN is required, it is a best

practice to include the tip during the transaction.

•

When an EMV card is tendered and signature is requested, the

customer can sign the receipt and tip is added later.

•

In the event that the customer card tendered only supports PIN

and the restaurant only supports “chip and signature” or no

customer verification method, restaurants may ask for another

form of tender.

How Are Cardholders Verified?

Use of PIN is a common EMV cardholder verification method (CVM)

that authenticates the cardholder and protects against the merchant’s

acceptance of a lost or stolen card. When a cardholder’s pin is

used to validate who they say they are, it is called “chip and PIN.”

In addition to chip and PIN, other customer verification methods

include signature verification and no customer verification, which

is used today at some quick service restaurants. The U.S. will most

likely migrate to “chip and choice,” which indicates PIN, signature

and no customer verification method. Selection of other appropriate

customer verification methods will depend on how customers pay

for goods and services at your location today, speed of checkout,

customer convenience, and the need for chargeback protection, as

well as the restaurant’s terminal or POS system’s capabilities.

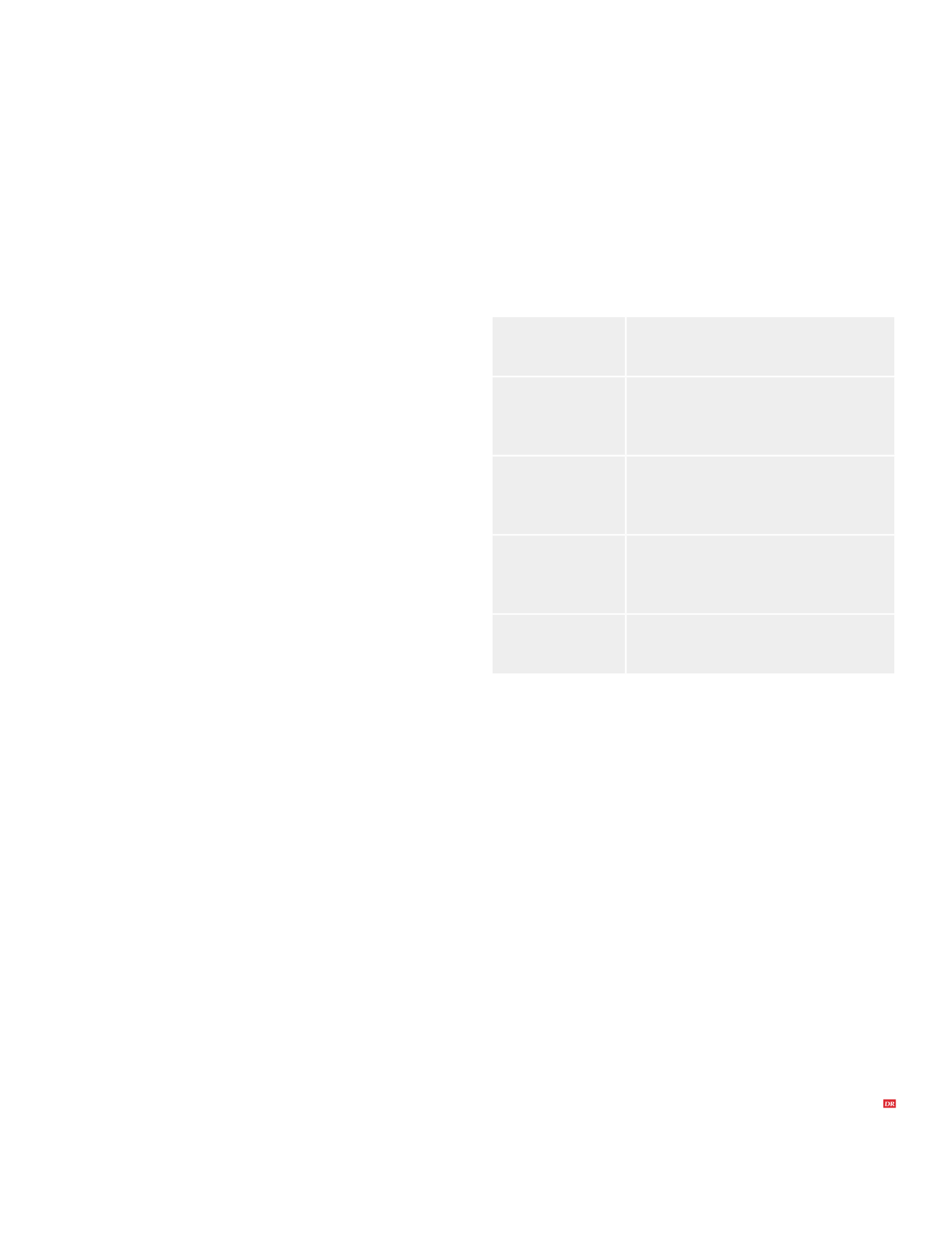

Customer Convenient Payment

The following are pay-at-the-table considerations for restaurants

implementing EMV:

What Is the Technology Innovation

Program (TIP) and Does It Apply to Me?

Effective October 2012, Visa’s TIP provides qualifying merchants—

Level 1 and Level 2 merchants that process more than 1 million

Visa transactions annually—PCI audit relief when 75% of the

merchant’s Visa transactions originate at a dual-interface EMV

chip-enabled terminal. However, all merchants must continue to

comply with PCI DSS. MasterCard offers a similar program to Visa.

It is important to note that whether you are a Level 1 merchant

processing more than 1 million transactions a year, or a restaurant

processing 10,000 transactions annually, you are still responsible

for being PCI compliant.

Questions?

If you have questions about EMV, lowering your cost of payments, how

to better manage your store network, improving transaction security,

payroll management or anything related to payment processing, please

reach out to us a

CHIP AND SIGNATURE

n

Follows current payment process

n

Minimal expense

STAND-BESIDE

PAYMENT

n

Purpose-built unit with EMV and NFC

n

Wallet acceptance

n

Stand-beside or semi-integrated

KIOSK AT THE TABLE

n

Requires iPad or Android at each table with

enclosure and readers

n

Power, battery life and security are concerns

PURPOSE-BUILT

MOBILE

n

Smartphone and sled, which is a cover encasing

the smartphone to provide payment acceptance

n

Integrated with POS system or stand-beside

MOBILE DEVICE

FOR ORDERING

AND PAYMENT

n

Smartphone and sled

n

Integrated with POS system